Options Data

Navigate Volatility with Confidence

From subtle shifts to dramatic market swings, Market Data prepares you to tackle volatility like a pro. Dive deep into options with clarity and precision, backed by our robust data.

Market Data Options APIs

Simple To Use, Effortless Configuration, Advanced Filtering

Download full option chains, use sophisticated filtering, get real-time or historical data with our robust options APIs, tailored for every requirement. Gain a competitive edge with our detailed and responsive data solutions.

Quotes With More Than Just Bid & Ask

Detailed real-time or historical (end of day) options quotes with a single easy-to-use endpoint. Keep up with the price, but see beyond it.

- Full level 1 quote for all US-listed options

- Greeks & implied volatility for all real-time quotes

- Last trade price included

- Open interest & volume data

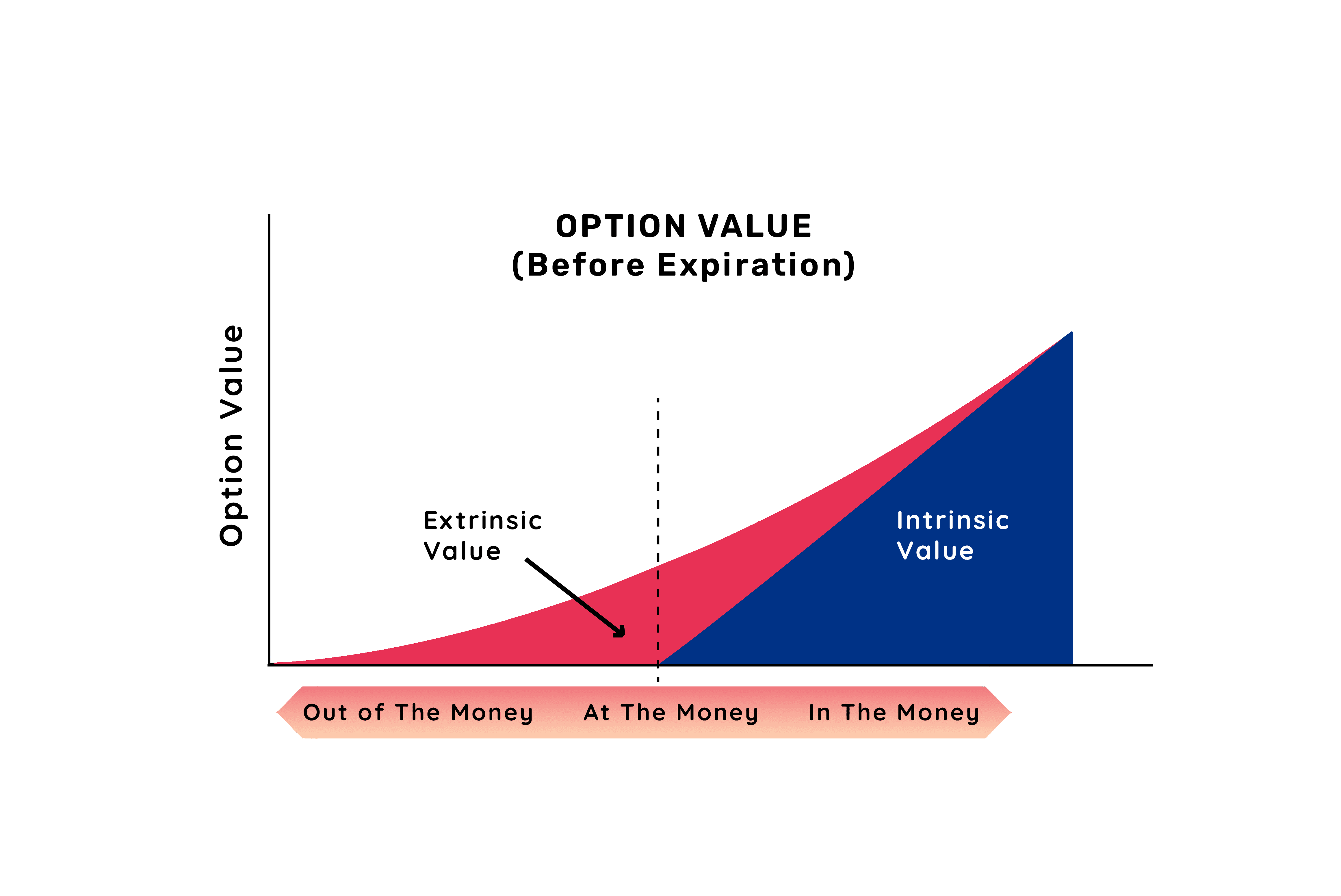

- Underlying price, intrinsic & extrinsic values included

- First-traded date included for easy historical follow-up requests

{

"s": "ok",

"updated": [1693588294],

"optionSymbol": ["AAPL230915C00200000"],

"underlying": ["AAPL"],

"expiration": [1694808000],

"side": ["call"],

"strike": [200.0],

"firstTraded": [1626787800],

"dte": [14],

"bid": [0.23],

"bidSize": [1044],

"mid": [0.24],

"ask": [0.24],

"askSize": [623],

"last": [0.24],

"openInterest": [54331],

"volume": [8211],

"inTheMoney": [false],

"intrinsicValue": [0.0],

"extrinsicValue": [0.24],

"underlyingPrice": [189.0],

"iv": [0.187],

"delta": [0.075],

"gamma": [0.02],

"theta": [-0.036],

"vega": [0.054],

"rho": [0.006]

}The World's Most Configurable Option Chain Endpoint

Save weeks of coding time by integrating our option chain API into your application. Every filter you think you need to code has already been built by our team. Get the exact contracts you need with no code necessary.

- Get real-time or historical (EOD) chains

- Filter by expiration, year, month, weekly quarterly

- Filter for standard or non-standard contracts

- Include or exclude strikes by dollar value or delta

- Set min or max values for bid/ask

- Filter out contracts with excessive bid/ask spreads

- Set thresholds for volume or open interest

{

"s": "ok",

"updated": [1693588212, 1693588212, 1693588212, 1693588212],

"optionSymbol": [

"AAPL230915C00187500", "AAPL230915C00190000",

"AAPL230915P00187500", "AAPL230915P00190000"

],

"underlying": ["AAPL", "AAPL", "AAPL", "AAPL"],

"expiration": [1694808000, 1694808000, 1694808000, 1694808000],

"side": ["call", "call", "put", "put"],

"strike": [187.5, 190.0, 187.5, 190.0],

"firstTraded": [1692624600, 1626787800, 1692624600, 1626787800],

"dte": [14, 14, 14, 14],

"bid": [3.65, 2.33, 1.87, 3.0],

"bidSize": [994, 170, 81, 302],

"mid": [3.7, 2.34, 1.88, 3.02],

"ask": [3.75, 2.34, 1.88, 3.05],

"askSize": [1052, 255, 233, 1112],

"last": [3.7, 2.32, 1.86, 2.98],

"openInterest": [17481, 57216, 8077, 19092],

"volume": [3470, 17475, 4293, 7403],

"inTheMoney": [true, false, false, true],

"intrinsicValue": [1.47, 0.0, 0.0, 1.03],

"extrinsicValue": [2.23, 2.34, 1.88, 1.99],

"underlyingPrice": [188.97, 188.97, 188.97, 188.97],

"iv": [0.178, 0.176, 0.178, 0.176],

"delta": [0.613, 0.466, -0.389, -0.538],

"gamma": [0.057, 0.06, 0.058, 0.061],

"theta": [-0.101, -0.1, -0.079, -0.079],

"vega": [0.145, 0.15, 0.145, 0.15],

"rho": [0.045, 0.034, -0.029, -0.038]

}Find Out When Options Are Expiring

Get a complete list of an underlying's available expiration dates quickly. Make historical requests using the same endpoint to find out when options expired in the past.

- Returns all future expirations

- Get a historical list of expiration dates from a specific previous trading day

- Filter to include only expirations with a specific strike

{

"s": "ok",

"expirations": [

"2024-05-17",

"2024-05-24",

"2024-05-31",

"2024-06-07",

"2024-06-14",

"2024-06-21",

"2024-06-28",

"2024-07-19",

"2024-08-16",

"2024-09-20",

"2024-10-18",

"2024-11-15",

"2024-12-20",

"2025-01-17",

"2025-03-21",

"2025-06-20",

"2025-09-19",

"2025-12-19",

"2026-01-16",

"2026-06-18",

"2026-12-18"

],

"updated": 1715866180

}Get Every Strike For Each Expiration

The Strikes API gives you the complete structure of the option chain with a minimal response size. Browse the option chain without the need to download every contract.

- Get the full option chain structure with a lightweight response size

- Returns strikes for all expirations

- Query a historical list of strikes dates from a specific previous trading day

- Filter to include only strikes from a specific expiration date

{

"s": "ok",

"updated": 1663704000,

"2023-01-20": [

30.0, 35.0, 40.0, 50.0,

55.0, 60.0, 65.0, 70.0,

75.0, 80.0, 85.0, 90.0,

95.0, 100.0, 105.0, 110.0,

115.0, 120.0, 125.0, 130.0,

135.0, 140.0, 145.0, 150.0,

155.0, 160.0, 165.0, 170.0,

175.0, 180.0, 185.0, 190.0,

195.0, 200.0, 205.0, 210.0,

215.0, 220.0, 225.0, 230.0,

235.0, 240.0, 245.0, 250.0,

260.0, 270.0, 280.0, 290.0,

300.0

]

}Lookup Option Symbols Using Natural Language

Lookup option symbols using text like 'AAPL Jan $200 Call' instead of AAPL250117C00200000. Convert proprietary output from broker platforms to industry-standard option symbols.

- Compatible with all major broker CSV formats

- No specific ordering or format is required

- Defaults to monthly expirations when dates are incomplete

{

"s": "ok",

"optionSymbol": "AAPL250117C00200000"

}The OPTIONDATA Formula

The Do-It-All Formula for Options Data

Designed for both real-time quotes and historical end of day quotes, OPTIONDATA is fully configurable and provides pricing data, greeks, implied volatility, and contract details for every option trading in the US. The OPTIONDATA formula is your Swiss Army knife for financial insights.

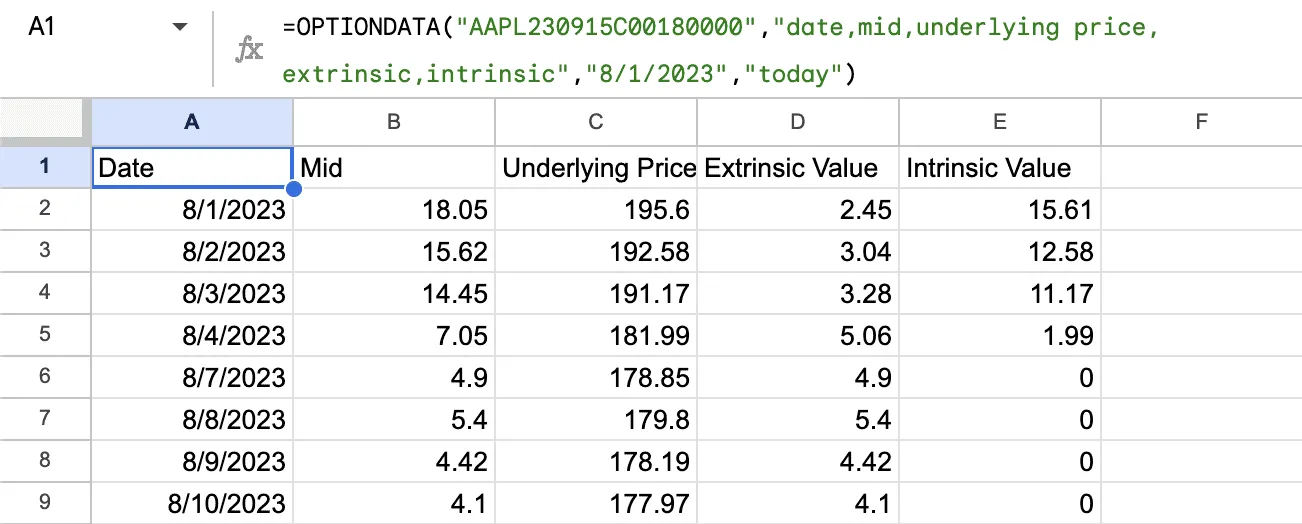

OPTIONDATA with relative dates for automatic updating

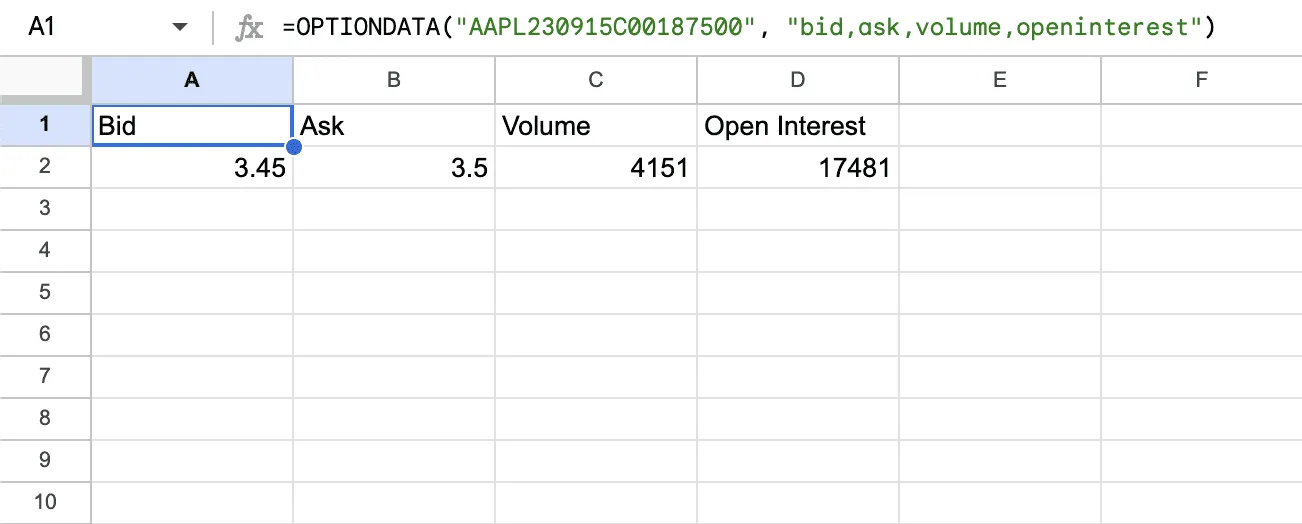

OPTIONDATA with custom column output

Begin Working With Options Data

Unlock the full potential of our options data with these quickstart tutorials for Google Sheets and the Market Data API. View all

How To Calculate Option Greeks In Your Spreadsheet

The OPTIONDATA formula will calculate the option greeks to your spreadsheet automatically using the keyword "greeks" as a parameter. Risk management has never b

How To Get An Earnings Calendar For Any Stock In Google Sheets

Add an earnings calendar to Google Sheets using Market Data's EARNINGS formula. Find what Wall Street Analysts are projecting for next quarter.

Candles vs Quotes, What’s The Difference?

What's the difference between candles vs quotes when it comes to stock data? Market Data offers both candlestick and quote data, so make sure you use the right

How To Get An Option Chain In Google Sheets

Use the OPTIONCHAIN formula to get a complete real-time option chain in Google Sheets. Filter by date, days to expiration, strike, deltas, and more.

How To Get Historical Options Prices For Your Spreadsheet

Using the Market Data Add-on, it is possible to get historical options prices going back decades directly into your spreadsheet with a simple formula.

How To Get Real-Time Stock Prices in Google Sheets

The GOOGLEFINANCE formula gives 15-min delayed stock prices. Get real-time stock prices into Google Sheets using the STOCKDATA formula.

How To Calculate Implied Volatility In Your Spreadsheet

Using the OPTIONDATA formula, you can calculate implied volatility for any option.

How To Build A Covered Call Spreadsheet

Learn how to build a covered call spreadsheet to track all your covered calls. Download our free covered call tracking spreadsheet example sheet for Google Shee

How To Get Options Prices in Google Sheets

Learn how to add real-time and historical options prices into your Google Sheets spreadsheets using a single formula.

How To Bulk Download Stock Data in Google Sheets

Learn how to perform bulk stock data downloads using Market Data's Google Sheets Add-on.

How to Calculate Theta For An Option

Learn how to calculate theta and understand how to add time decay to your spreadsheets.

How To Calculate The Intrinsic / Extrinsic Value of an Option In Your Spreadsheet

Using the OPTIONDATA formula, you can automatically calculate the implied volatility of any option that is currently trading.